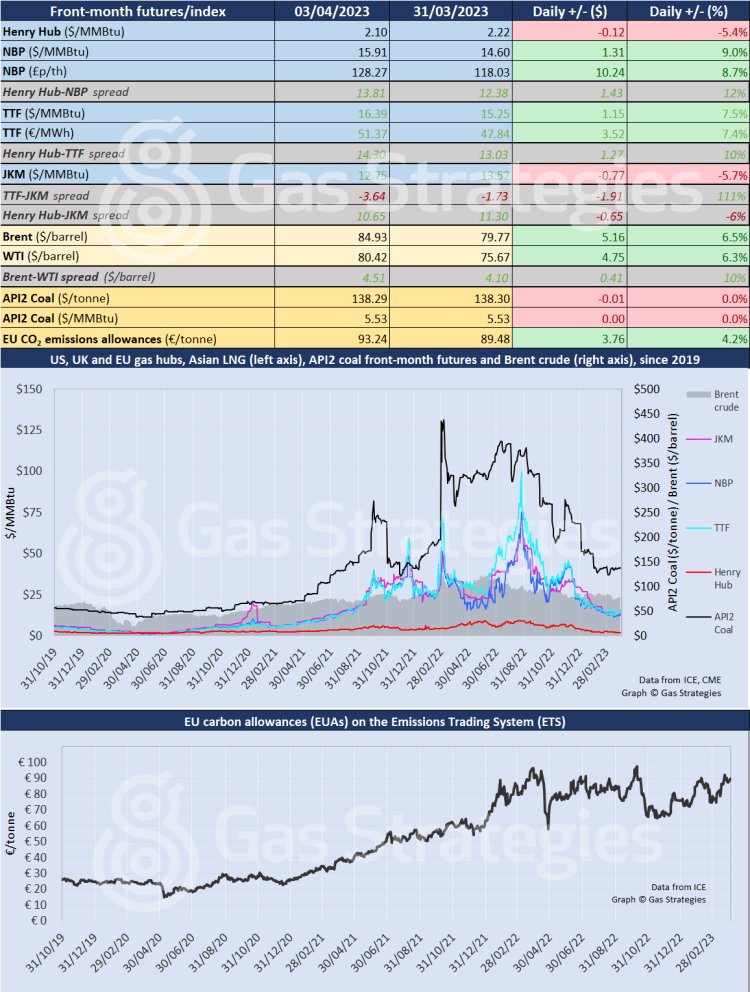

European natural gas prices continued gaining ground on Monday, as a surprise decision by OPEC+ over the weekend to continue cutting production kept pressure on commodity prices.

The decision of OPEC+ to cut another 1.1 million barrels/d on top of reduced Russian output and the group’s previously announced cuts pushed Brent prices higher Monday. Brent shot up 6.5% to USD 84.93/barrel and WTI saw a 6.3% rise to USD 80.42/barrel.

While European natural gas inventories continue being at their highest level in over a decade – 56% full as of 2 April, according to GIE – the market continues being sensitive to any potential supply threat as the continent continues to wean itself off Russia’s energy.

Accordingly, the UK’s NBP price saw a 9% surge to USD 15.91/MMBtu, while TTF in the Netherlands soared 7.5% to USD 16.39/MMBtu.

Meanwhile, the Asian LNG market JKM dipped 5.7% to USD 12.75/MMBtu, leaving TTF at a significant USD 3.64 premium over JKM.

The European Union Agency for the Cooperation of Energy Regulators (ACER) reported its first LNG benchmark price last Friday. ACER reported benchmark LNG in Europe was trading at a USD 3.06/MMBtu discount to TTF, with the price of LNG delivered ex-ship to Europe assessed at USD 12.20/MMBtu.

In the US, Henry Hub fell Monday due to continued pressure from strong production, modest demand and heavy storage supplies.

The price slipped 5.4% to USD 2.10/MMBtu.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):  Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.